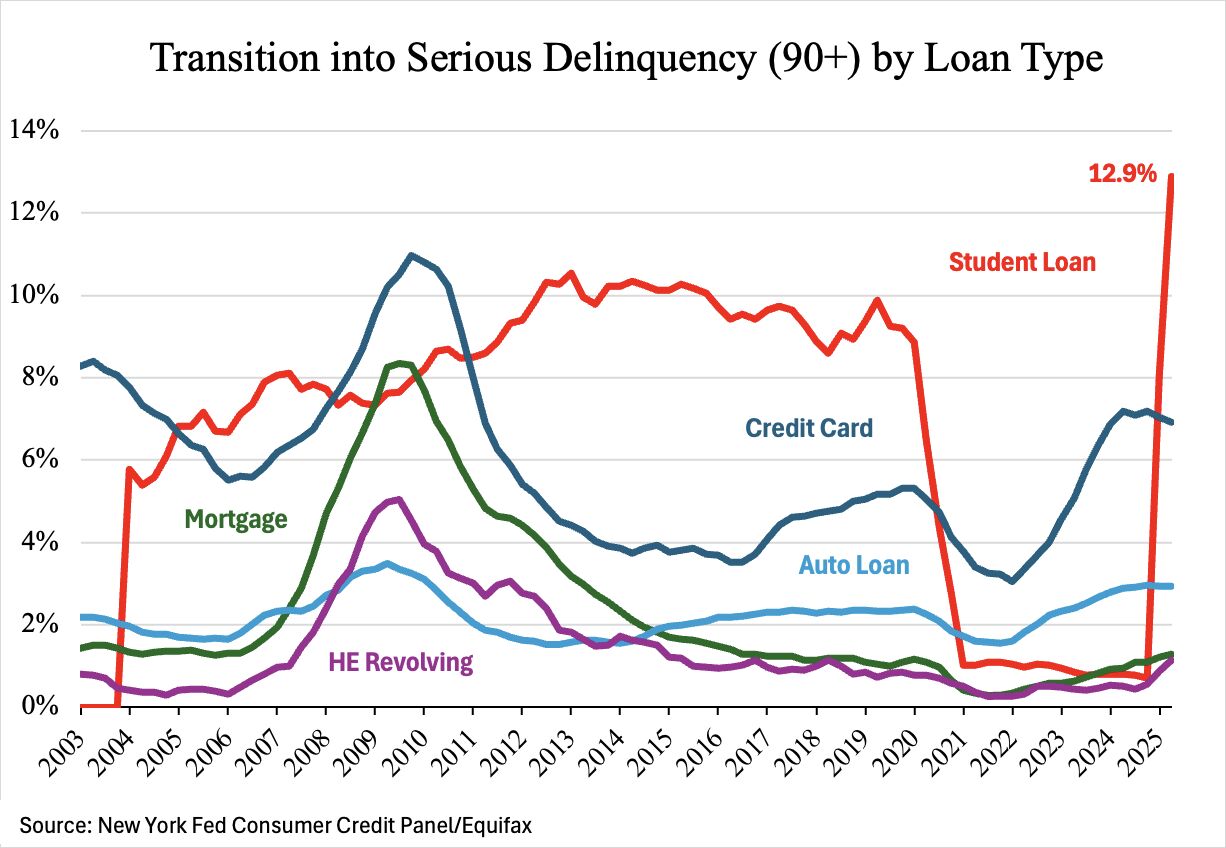

Imagine the U.S. consumer credit market as a steady vessel navigating a changing financial landscape. While most compartments remain secure, one is now showing signs of strain: student loans. Following the end of pandemic-era payment suspensions, serious delinquencies among student loans have jumped to 12.9%, marking the highest rate seen in the past 21 years. This sharp rise has fueled anxiety about household debt and the risk of a broader crisis.

But a closer examination of the market presents a more balanced perspective:

- Student loans account for just 9% of total household debt – meaning their impact, though significant for affected borrowers, does not determine the overall health of the market.

- By contrast, the backbone of household debt – mortgages, auto loans, and credit cards – which represent nearly 90% of all consumer borrowing, continue to show relatively steady or only modestly increased delinquency rates.

- Credit availability is on the rise, with new mortgage originations, auto loans, and credit card limits all increasing. In Q2, lenders demonstrated confidence in household capacity by expanding access to credit and supporting ongoing consumer spending.

The current spike in student loan delinquencies reflects a one-off adjustment as repayment schedules and reporting return to normal after almost five years of paused obligations. For consumers as a whole, borrowing and repayment remain disciplined, and the majority of payments continue to be made on time.

The Big Picture

Despite genuine concern for student loan holders, the broader credit market shows strength and resilience. Households are, on the whole, successfully managing obligations, spending confidently, and pursuing new credit opportunities. The narrative of crisis is limited to one sector, while the vessel of the U.S. credit market continues to move forward.

Let’s Talk

If your business is focused on consumer or retail and is looking to raise capital, Bankers Edge Advisory is here to help you see past the headlines and connect with investors who understand the true nature of today’s credit landscape.