What if everything you learned about oil prices and the economy is wrong?

I ran some simple math this weekend and the numbers surprised me.

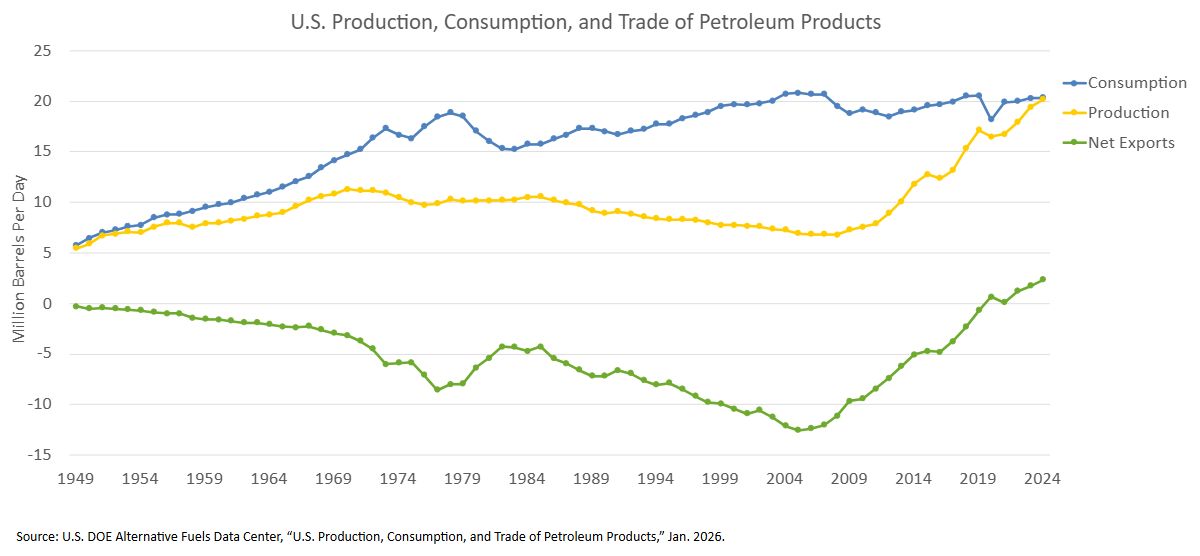

We’ve been taught that higher oil prices hurt American consumers. That was true – when we were a net importer of oil. But that world doesn’t exist anymore.

Today, the US produces 13.6 million barrels per day. We’re the world’s largest crude oil producer.

At $100/barrel, domestic production generates ~$469B in annual revenue. Total household energy spending across 130M US households ~$437B.

Production revenue now exceeds the entire consumer energy burden by $62B – before multiplier effects from jobs, drilling, and state tax revenue.

Moreover, the money stays home. In the 2000s, oil spikes meant hundreds of billions flowing to Saudi Arabia, Venezuela and Russia. Today it recirculates locally – wages, royalties, equipment orders, state budgets.

In addition, recent tax legislation blunts whatever consumer sting remains, putting ~$2,900 back into household pockets. Those tax savings more than offset the energy cost increase so long as oil stays below $150.

The US economy now has a structural long position in oil.

So at what price does higher oil actually start to hurt America? I’d argue it’s a lot higher than most people think.

I would argue higher mortgage rates more negatively impact the US economy than higher oil prices. And unlike oil, where the US now has offsetting production gains, there’s no comparable domestic “long position” in higher rates – they’re almost purely contractionary for household and business capital formation.

Richard Consul, CFA | Mitch Vermet, CFA, CAIA